As an employee, you don’t need to put much thought into which taxes are taken out of your paycheck after you’ve set up your specific withholdings, e.g. health insurance, Flex Spending Account, Retirement, and other pre-tax fringe benefits that reduce your taxable income. Even then, your employer’s payroll system and initial questionnaire forms usually make your W-2 “tax configuration” easy and streamlined for you. If you take a closer look at your earnings on your pay stub and W-2, you will then see automatic tax withholdings for things like Social Security, Medicare, federal taxes, local city (SDI in California) and state income taxes.

When you make the jump from employee to self-employed, you’re required to pay these taxes 100% on your own. You may choose to use a payroll system like Gusto or ADP which handles much of this for you with little pain on your end besides the money that gets taken for taxes. If you are strictly 1099 and do not run payroll, or need to configure or reconfigure your payroll setup, you want to make sure that you’re contributing correctly. Here are a few key points of which you need to be made aware.

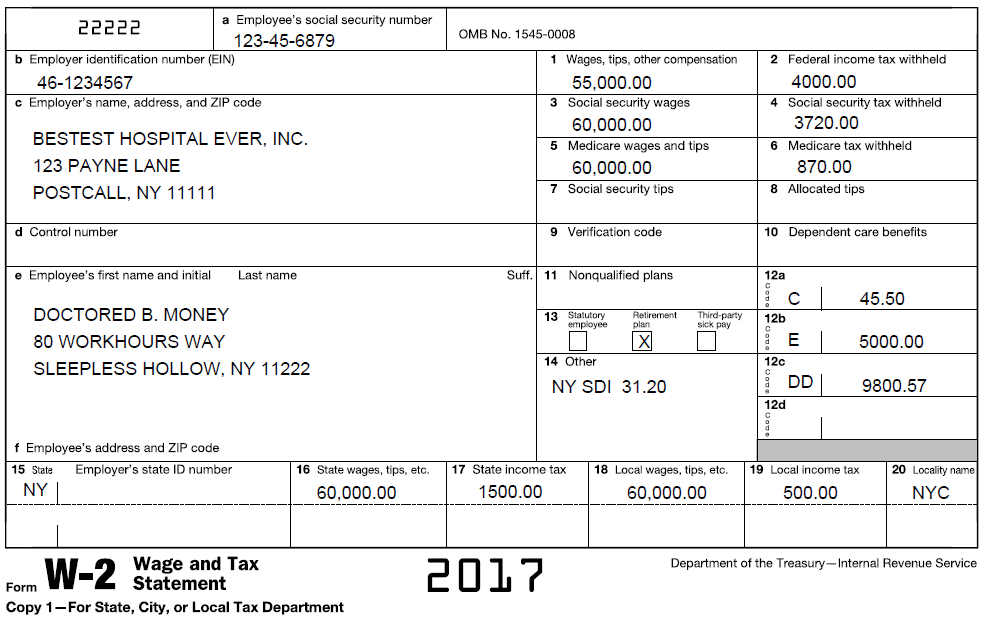

What is W-2 income?

A W-2 tax form shows you essential information about the income you’ve received from an employer over a one-year period. It shows the amount of taxes that have been withheld, the benefits you’ve received, and it enables you to file your federal and state income taxes. Generally, if you’ve worked as an employee you should receive a W-2 form from your employer at the end of January.

Only those who have worked as an employee receive a W-2. Additionally, if you have a large enough operation of your own, or have designed an advanced tax strategy, you may run your own payroll even if you are the sole employee. The majority of our LLC and S Corp clients should expect to pay themselves payroll in the first few years.

What is 1099 income?

When you work for yourself in an Inc. or LLC or as a sole proprietor/independent contractor, you receive a 1099 tax form instead of a W-2. 1099 forms also show important information about the income you’ve received from different sources over the year. As a self-employed person, you’ll receive a 1099-NEC (1099-MISC in 2019 and prior) form instead of a W-2.

You can expect to receive this form from a client or business that has paid you more than $600 for your product or services over the course of a given year. Like the W-2, you’ll receive these forms at the end of January.

The biggest difference between the two forms is that a W-2 shows you the taxes that have been withheld from your pay, while a 1099-NEC doesn’t. That’s because an independent contractor (or, a self-employed person) is required to pay taxes on their own. This is called a self-employment tax.

What is self-employment tax?

Alas, being self-employed does not mean that you’re exempt from paying taxes. The self-employment tax is the tax that independent contractors and Solopreneurs are required to pay on their income.

Note that the US taxes all employees a total of 15.3%. The rate consists of two parts: 12.4% for Social Security (old-age, survivors, and disability insurance) and 2.9% for Medicare (hospital insurance).

In the employee-employer relationship (e.g. W-2 wages as a full-time employee of a company) your employer pays half of this – you won’t even see that however on any document or W-2 or wage statement/pay stub.

In the below example you’ll see that Social Security and Medicare is taken off the $60,000 wages at half of the above examples – 6.2% and 1.45%. You won’t see it or probably know it, but the employer is paying the other half of the 12.4% of Social Security and 2.9% medicare.

If you’re still following, you can guess that when an employer is absent and you are considered self-employed, you’re on the hook to withhold and transmit the entirety of the 15.3% on all net profit of business income. For simplicity’s sake, the IRS 1040 federal return simply calls this a “self-employment tax” on form Schedule SE.

And if you are interested, here’s the exact breakdown:

In 2021, the first $142,800 of your net earnings is subject to the Social Security portion of the self-employment tax. For example, if you earned $150,000 net profit from self-employment, you have to pay 12.4% on $142,800, but you’re not required to pay that percentage on the remaining $7,200.

However, for the Medicare portion (2.9%), you’re required to pay that percentage on the full $150,000. And, if you earn more than $200,000 (as an individual), you’re subjected to an additional 0.9% Medicare surtax. For example, if you earn $250,000 this year, you’ll have to pay 2.9% to Medicare on $200,0000, and an additional 0.9% surcharge on the remaining $50,000.

What are estimated taxes?

As a self-employed person, your taxes aren’t automatically withheld. That means that you’re required to pay estimated taxes based on your taxable profits every quarter. You can use IRS form 1040-ES to determine how much you owe.

The payments are due on the following dates (if the date falls on a weekend or a holiday, it is automatically pushed to the next business day):

- April 15

- June 15

- September 15

- January 15

You can pay your estimated taxes by filling out the 1040-ES form and sending a check to the U.S. Treasury, or you can use the IRS website to make your payments online. Alternatively, you can also use the Electronic Federal Tax Payment System (EFTPS) to schedule your estimated payments for up to a year in advance. Fortunately, the interest and fees applied to late or misestimated taxes are not significant.

There is a totally legal loophole that you can make the most of if you prefer to pay your IRS and state taxes together on December 31 of the given year. Solosherpa can help you learn how to utilize a payroll tool so that you can take advantage of it!

Who is required to pay self-employment tax?

You are required to pay self-employment taxes if you earn more than $400 in net profit in a given year. This applies to Solopreneurs, independent contractors, and freelancers. And, if you have a full-time job but have earned over $400 from a side hustle, you’ll have to pay as well.

There are very few ways to avoid paying the government 15.3% on income and profit. One of the only legal ways to do so is to set up a formal, legal employment arrangement. This arrangement enables the owner of a corporation to choose to pay themselves a wage and return remaining profits back to themselves as owners disbursements and return on investment that avoids the burdensome 15.3% tax.

Solopreneurs can almost always set this up, and the tax savings often come up to many thousands. Solosherpa helps our clients evaluate their corporate structure and determine the potential advantages and steps to legally minimize self-employment taxes. Contact us now for assistance!

Photo by The New York Public Library on Unsplash